Life settlements feel like a modern financial innovation, but the legal and economic principles that make them possible are over a century old. The story begins in 1911, in a Supreme Court courtroom, with a dispute over a single insurance policy purchased for the price of a doctor’s bill. That ruling, almost forgotten outside legal circles, quietly established the foundation for one of today’s most distinctive alternative asset classes.

Grigsby v. Russell: the case that started it all

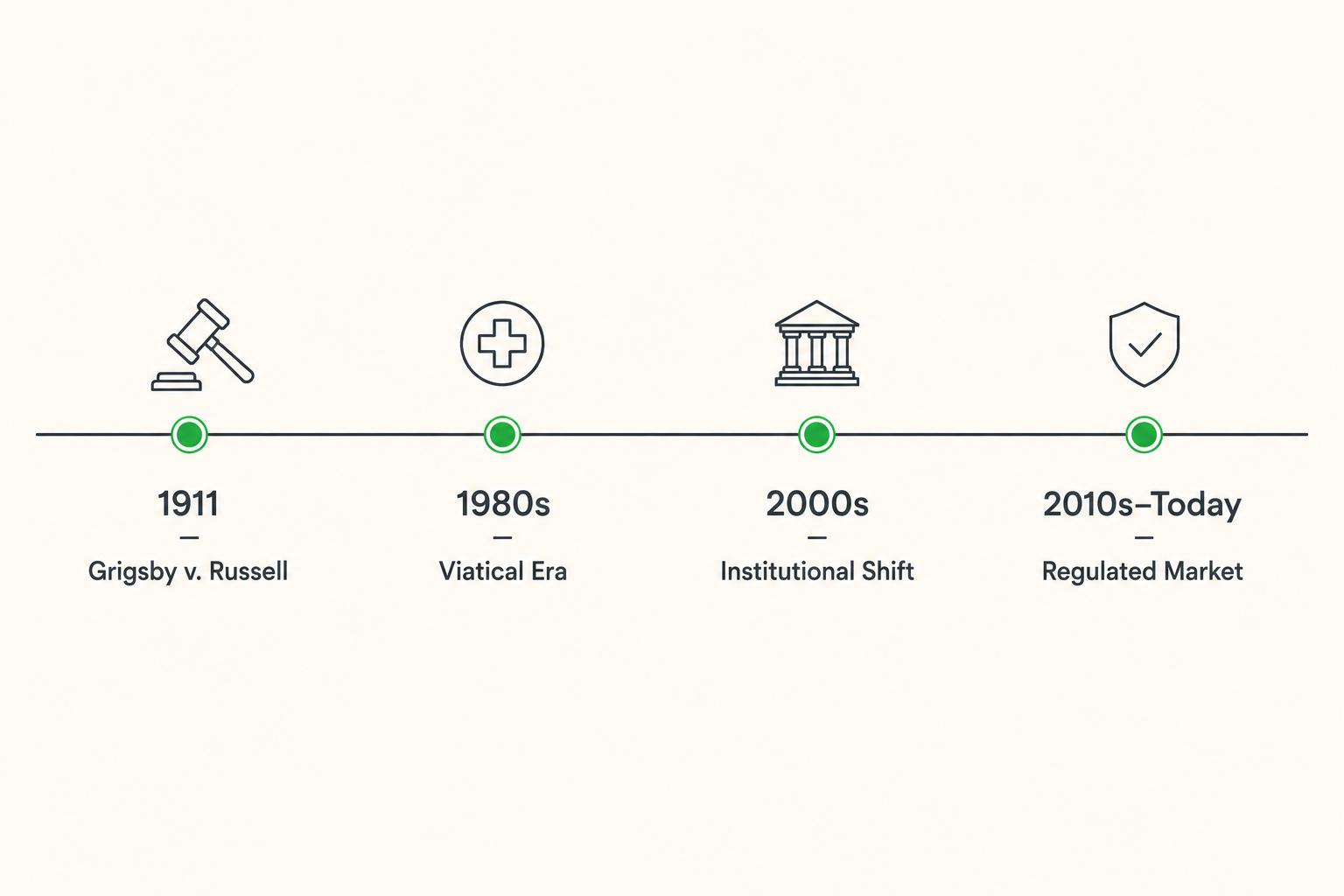

In 1911, the U.S. Supreme Court heard the case of Grigsby v. Russell. A man named John Burchard, in poor health and unable to pay the premiums on his life insurance policy, sold the policy to his physician, Dr. A.H. Grigsby, in exchange for $100 and an agreement that the doctor would continue paying the premiums. When Burchard died, a dispute arose over who was entitled to the death benefit.

Justice Oliver Wendell Holmes, Jr., writing for the Court, ruled that a life insurance policy is personal property, and like any personal property, it can be sold or assigned to another party. "So far as reasonable safety permits," Holmes wrote, "it is desirable to give to life policies the ordinary characteristics of property." That single sentence established the legal foundation for the entire secondary market in life insurance that exists today.

“So far as reasonable safety permits, it is desirable to give to life policies the ordinary characteristics of property.”

Decades of quiet existence

For most of the 20th century, the Grigsby ruling sat on the books with limited practical application. Policies were occasionally sold or transferred, but no organized secondary market emerged. Life insurance was something families bought and held; the idea of trading policies like securities was foreign to mainstream finance.

That began to change in the 1980s, but for a tragic reason. The AIDS epidemic created a population of younger policyholders facing dramatically shortened life expectancies, often without the financial resources to cover medical care. Selling a life insurance policy for cash today, rather than leaving it as a future benefit, offered immediate relief. The viatical market (the term comes from "viaticum," the Latin word for provisions for a journey) was born to serve this need.

The viatical era and its growing pains

The viatical market of the late 1980s and 1990s was the first organized secondary market for life insurance. It served a real human need, but it also operated largely outside meaningful regulation. Pricing was inconsistent, disclosures were incomplete, and a small number of bad actors gave the broader industry a reputation problem it would spend years working to fix.

As medical advances in the late 1990s extended life expectancies for many viatical sellers, returns to investors fell short of expectations, not because the model was broken, but because actuarial estimates had not kept pace with treatment breakthroughs. State regulators began to take notice, and by the early 2000s a wave of new state-level licensing requirements, disclosure rules, and consumer protections began to take shape.

The shift to senior life settlements

Around the same time, the market’s center of gravity shifted. Instead of younger viatical sellers with terminal illnesses, the typical seller became a senior (age 65 or older) who simply no longer needed the coverage they had purchased decades earlier. Estate planning needs had evolved. Children were grown. Premiums had become an unwelcome expense in retirement. The economics were different, the timelines were longer, and the actuarial science was more mature.

This new "senior life settlement" market attracted institutional capital. Pension funds, hedge funds, and large family offices recognized that pools of senior policies, diversified across many insureds, produced cash flows that were genuinely uncorrelated with everything else in their portfolios. The asset class began to grow up.

Regulation matures

Today, life settlements are regulated in 43 U.S. states plus Puerto Rico, covering well over 90% of the U.S. population. The National Association of Insurance Commissioners (NAIC) and the National Conference of Insurance Legislators (NCOIL) have both published model acts that most state regulations are based on. Brokers and providers are licensed. Consumer disclosures are mandated. Sellers have a statutory rescission period, typically 15 to 30 days, during which they can reverse the transaction with no penalty.

For investors, the regulatory maturity matters in two ways. It protects sellers (which protects the long-term reputation and supply of the asset class) and it provides a stable, predictable operating environment that institutional capital requires before it allocates at scale.

Where the market stands today

The U.S. life settlement market now transacts billions of dollars in face value each year. The Life Insurance Settlement Association (LISA) estimates that hundreds of billions of dollars in eligible policy face value lapse or surrender every year. Those are policies that could have been sold for materially more than their cash surrender value if their owners had known the option existed. That gap between awareness and opportunity is, in many ways, the modern story of the market.

On the investor side, what was once an exclusively institutional asset class is opening to accredited individuals. Platforms, fund structures, and operational tooling have evolved to support smaller commitments without compromising the underwriting and servicing discipline that made the institutional version work.

A century later

The thread that runs from Justice Holmes’s 1911 opinion to a 2026 portfolio allocation is simple: a life insurance policy is property, and like all property, it has a fair market value that the open market can discover. Every decade since has been a step toward making that market more transparent, more efficient, and more accessible. The asset class today is the culmination of that long, quiet evolution, and for investors who understand its history, that maturity is a feature, not an afterthought.