A life settlement is the sale of an existing life insurance policy to a third-party investor for more than the policy’s cash surrender value, but less than its eventual death benefit. For the seller, it unlocks immediate cash from a policy they no longer need or can afford. For the investor, it offers a contractually defined return when the insured passes away. The transaction is legal in every U.S. state and regulated in most of them, and it has quietly grown into a multi-billion-dollar institutional asset class over the past two decades.

If you’ve never heard of life settlements before, you’re not alone. The market has historically served pension funds, hedge funds, and family offices behind closed doors. But the underlying mechanics are straightforward, and understanding them is the first step to evaluating whether the asset class belongs in your portfolio.

What exactly is being sold?

A life insurance policy is a contract. The policyholder pays premiums, and in return, the insurance company pays a death benefit to a named beneficiary when the insured dies. Like any contract with future cash flows, that policy has economic value. Since a 1911 Supreme Court ruling, U.S. law has recognized life insurance as transferable personal property, so the policyholder can assign that contract to someone else for a price.

In a life settlement, the policyholder transfers ownership of the policy to an investor. The investor takes over premium payments going forward and becomes the new beneficiary. When the insured passes away, the death benefit is paid to the investor rather than the original beneficiary.

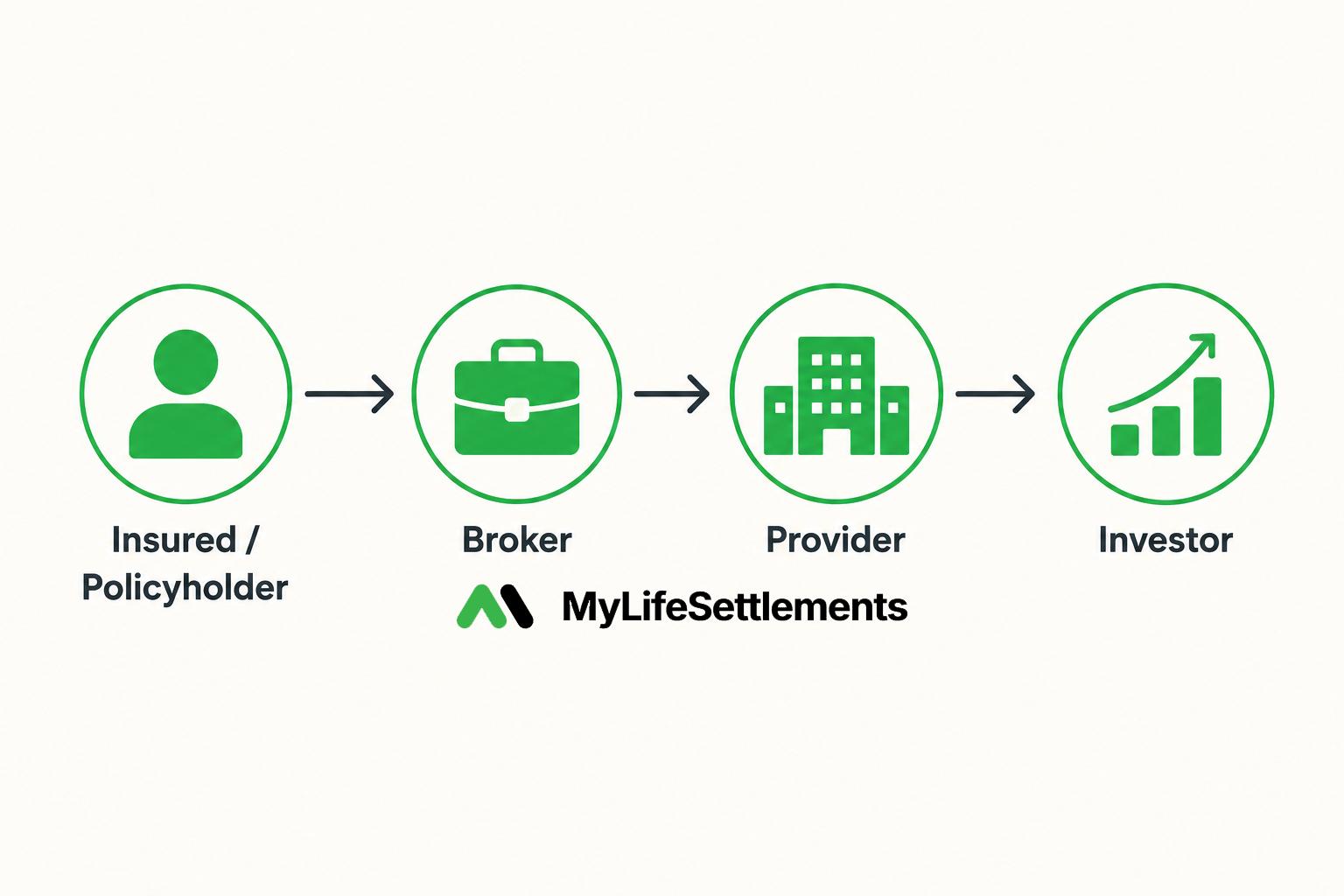

Who is involved in a transaction?

A typical life settlement involves four parties working in sequence:

- The insured (also called the policyholder) is typically a senior age 65 or older whose original need for the policy has changed. Maybe the children they were protecting are now grown and financially independent. Maybe premiums have become unaffordable. Maybe estate planning needs have shifted.

- The broker is a licensed intermediary who represents the policyholder, shops the policy to multiple buyers, and negotiates the best price on the seller’s behalf.

- The provider is a licensed buyer (often funded by institutional capital) who underwrites the policy, makes an offer, and handles the legal transfer of ownership.

- The investor is the ultimate owner of the policy, who funds the purchase and collects the death benefit when the policy matures.

Brokers and providers are typically licensed by the same state insurance regulators who license life insurance companies and agents. The transaction itself is governed by a settlement contract that the policyholder signs after being fully informed of the offer, their alternatives, and their right to rescind within a state-mandated window (often 15 to 30 days).

Why does the policy have value above its cash surrender value?

When a policyholder surrenders a policy back to the insurance company, they receive only the cash surrender value, a number set by the insurer that often reflects a small fraction of the policy’s true economic worth. The insurance company benefits when policies lapse or surrender, because it no longer owes the death benefit.

“A life settlement is, in essence, a fair-market alternative to surrendering a policy back to the insurer.”

A life settlement creates a competitive market for that policy. Investors are willing to pay more than surrender value because they can underwrite the insured’s actual life expectancy, model the future premium stream, and price the policy based on its expected cash flows. The result is typically several multiples of the cash surrender value paid to the seller, a meaningful financial outcome for someone who no longer needs the coverage.

How do investors earn a return?

The investor’s return is mechanical: they pay a purchase price up front, continue paying premiums for the life of the policy, and receive the full death benefit when the insured passes away. The difference between those cash outflows (purchase + ongoing premiums) and the eventual death benefit is the gross return. Spread it over the expected duration of the policy, and you get an annualized internal rate of return.

Two things make this return profile unusual. First, the death benefit itself is fixed and contractually guaranteed by a regulated U.S. life insurance carrier, the same kind of carrier that backs the policies in your own portfolio. Second, the timing of the payout is governed by mortality, not by interest rates, equity markets, or credit cycles. That is the source of the much-discussed "non-correlation" of life settlements as an asset class.

The risks worth understanding

Like any asset class, life settlements carry risks. The biggest is longevity risk. If the insured lives substantially longer than estimated, the investor pays premiums for longer and the annualized return decreases. Diversified portfolios of policies mitigate this risk by averaging actual mortality across many lives. Premium maintenance is also critical: missing a premium payment can cause a policy to lapse, destroying its value entirely. Reputable funds and platforms have dedicated servicing operations to ensure this never happens.

There is also liquidity risk. A life settlement is not a publicly traded security, and policies are typically held to maturity. Investors should treat the asset class as a long-duration, illiquid allocation, similar to private credit or private equity.

The bottom line

A life settlement turns an underperforming insurance policy into a meaningful payout for the seller and a contractually defined investment for the buyer. The mechanics are simple. The regulation is mature. And the asset class has, for years, delivered the kind of non-correlated, contractually backed returns that institutional investors structure entire portfolios around. The rest of our Learn series goes deeper into the investment case and the history that brought us here.